Weekly Briefing: Tariffs, Tapers, and Trendlines

Weekly Roadmap for 03/16-03/22

Volatility Persists, but a Countertrend Rally May Be on the Horizon

Another week, another dose of headline-driven volatility. Uncertainty around tariffs and broader policy decisions kept markets on edge, kicking off with a weekend interview on Fox Business where former President Trump reiterated his stance on trade. As the week progressed, tensions flared between the U.S., Canada, and Europe over tariffs, fueling market swings. However, by Friday, signs of progress between the U.S. and Canada helped spark a relief rally, softening some of the week’s earlier losses.

Despite the late-week bounce, it was still a rough stretch for equities. The Dow led the declines, dropping nearly 3%, while small caps—despite holding up better—still finished down over 1.6%.

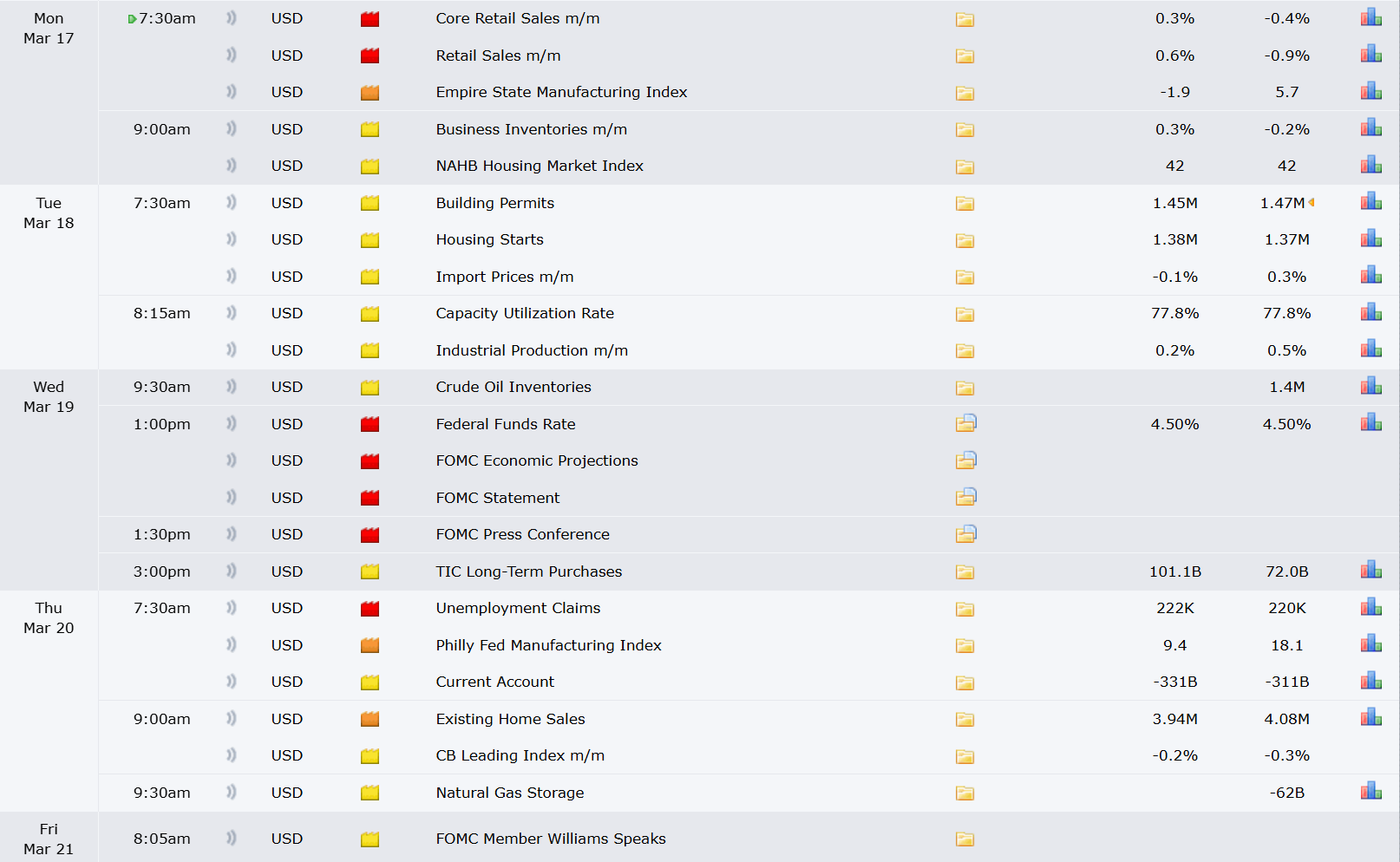

Key Economic Events This Week

Looking ahead, it’s a relatively light week for economic data. We’ve got retail sales on Monday and the usual jobless claims on Thursday, but the real focus will be on the FOMC meeting Wednesday. The Fed is widely expected to hold rates steady, with the first projected cut of 2025 still penciled in for June. Just a few months ago, markets were barely pricing in a single cut for the year—now, expectations have risen to three.

Last Week’s Volatility: What Drove the Market?

A mix of political uncertainty and tariff concerns fueled the market's swings. Trump’s Fox Business interview reinforced several key points:

Tariffs may increase further

The economy is in a transition phase

Trump isn’t concerned about the stock market

The administration wants lower interest rates

Monday’s reaction was swift—deleveraging hit hard, triggering the largest two-day selloff in four years. As the week progressed, the tariff back-and-forth between the U.S. and Canada added to the uncertainty:

Early in the week: Trump announced plans to raise steel and aluminum tariffs on Canada to 50%.

Midweek: A reversal—Trump suggested he might roll back the increase.

By Friday: Talks between the U.S. and Canada seemed more constructive, helping ease market fears.

While this uncertainty dominated headlines, inflation data provided a different narrative. Both CPI and PPI came in softer than expected, easing concerns about overheating. However, the details of PPI raised some caution flags—certain components that feed into PCE inflation came in hotter than expected, leading to upward revisions in PCE estimates. This slightly weighed on bonds, despite the overall positive inflation readings.

Are Markets Due for a Rebound?