Weekly Briefing: Tariff Tensions, Jobs Data, and the Battle for Growth

Weekly Roadmap for 03/02-03/08

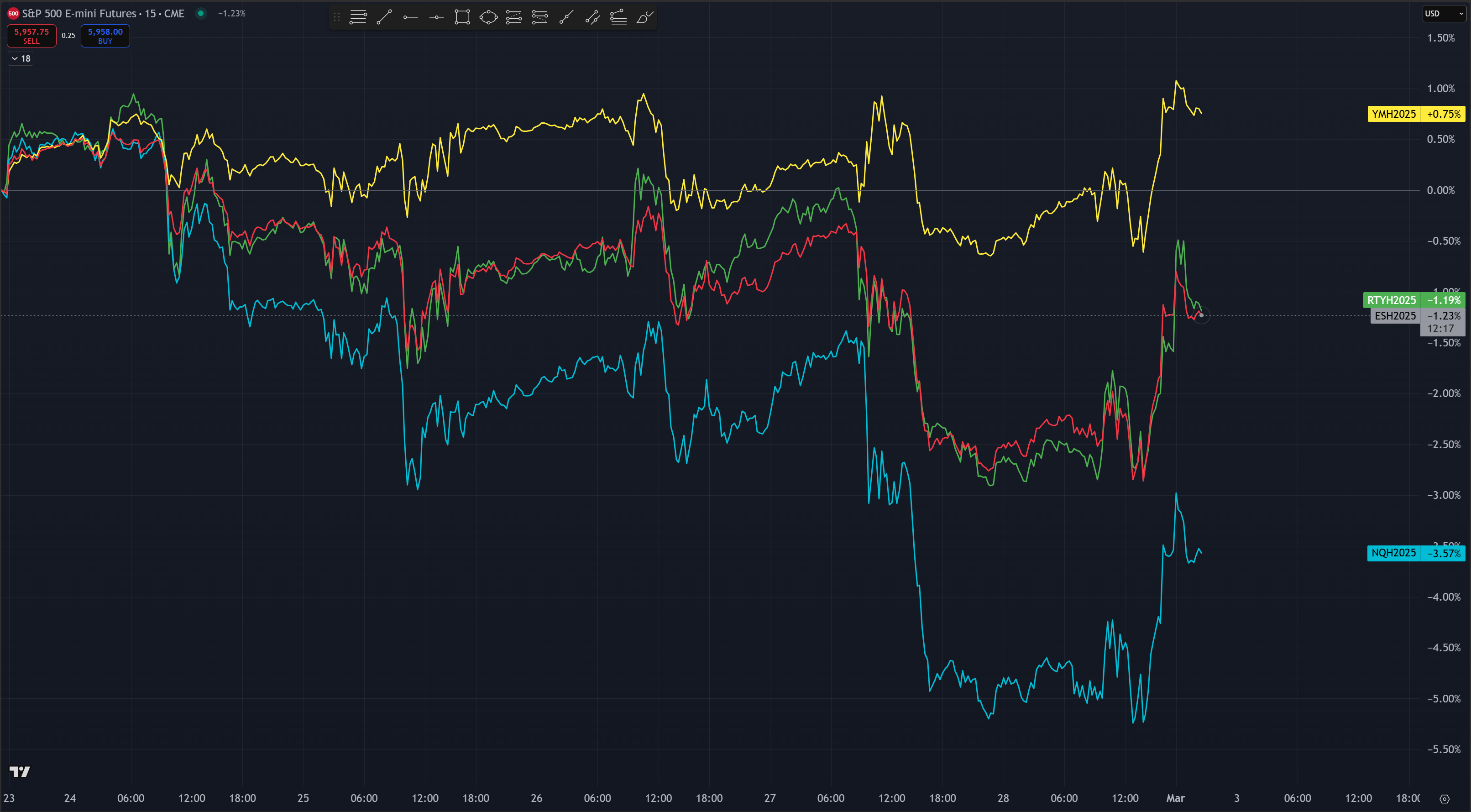

Market Recap: A Volatile Week in Review

This past week was a rollercoaster, with markets grappling with a continued unwind of momentum trades. High-beta stocks, particularly in tech, bore the brunt of the pressure, while defensive sectors and bonds saw a rotation as investors sought safer ground.

The Nasdaq 100 (QQQ) was the worst-performing index of the week, sliding over 3.3%, largely due to the post-earnings selloff in Nvidia (NVDA) and broader weakness in semiconductors and the Magnificent 7 stocks. On the flip side, defensive plays in financials and industrials helped the Dow Jones (DJIA) emerge as the best performer, gaining just under 1% for the week.

Recap of last weeks Trades:

We added 2 new trades last week as well as getting long BTC.

You can find the write ups here:

Key Economic Data to Watch This Week

The upcoming week is pivotal, with a heavy dose of economic and jobs data in focus. Investors will be watching closely to see if recent concerns over slowing growth persist or if we get a reprieve. Here are the major catalysts:

Non-Farm Payrolls (NFP) – Friday

Expected: 133k jobs added vs. 143k prior

Unemployment rate forecast: 4.0% (unchanged)

Trump's Trade Tariff Deadline – Tuesday

The administration is set to implement tariffs on Mexico, Canada, and China unless a last-minute trade deal is reached.

Trump has stated he will lift tariffs if an agreement is secured, making this a crucial week for negotiations.

Market Drivers: Tariffs, Growth Concerns & Fiscal Policy

Last week’s momentum unwind was fueled by escalating growth fears, which were further exacerbated by comments from Treasury Secretary Bessent and ongoing trade tensions.

Bessent’s Key Statements & Market Takeaways

Targeting a 3% fiscal deficit-to-GDP ratio – Currently at 6.4%, making this an extremely ambitious goal.

Reducing government spending while easing monetary policy – Aligns with Trump’s stance on future rate cuts.

Shifting economic growth from government to the private sector – A major challenge, given that much of recent job growth has been government-driven.

This all ties into the Department of Government Efficiency (DOGE), which has already cut 117,880 federal jobs, impacting just 3.93% of total government employment. While these cuts have been significant, they are still minor relative to the broader labor market, meaning the market may be overreacting to these developments.

Trade War Cycle: Where Are We Now?

We seem to be in the “Market Sells Off on Trade-War Fears” phase, with the next step likely being “Hints of Resolution”—possibly as early as this week if negotiations progress.

Mexico & Canada: Historically cooperative, meaning a quick resolution is possible.

China: A trickier situation, especially after China’s retaliatory tariffs. Trump has threatened an additional 10% tariff if tensions escalate further.

Inflation Update: Positive Signs, But March Will Be Key

The Personal Consumption Expenditures (PCE) report showed progress on the inflation front:

Headline PCE: 2.5% vs. 2.6% prior

Core PCE: 2.6% vs. 2.9% prior

While encouraging, the next inflation print in March will be critical, as it’s the last major data point before the next FOMC meeting. Inflation has been running hotter than expected, but this has been influenced by seasonality, tariffs, and economic disruptions (e.g., California wildfires, food inflation due to bird flu).

Market Technicals: Key Levels to Watch

Keep reading with a 7-day free trial

Subscribe to Blackshore’s Substack to keep reading this post and get 7 days of free access to the full post archives.